Industry updates | April 2023

Please take note of the following industry updates that may be relevant to you and your business.

COMPLIANCE AND ADMINISTRATION

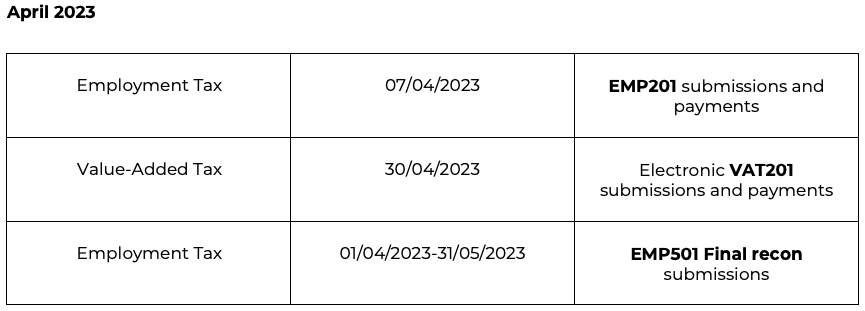

Due dates for reporting and payments- April 2023:

TAX ADMINISTRATION

1. Sharper focus put on the declaration of rental income for 2023/2024

Taxpayers are alerted to the fact that they should ensure that they declare any taxable rental income to SARS.

This warning is relevant not only to South African tax residents in respect of all their rental income, but also to non-residents in respect of rental earned from South African properties (South African source income).

In the case of a transfer of immovable property that is situated in South Africa, the transfer duty receipt from SARS must be registered at the Deeds Office. The Deeds Office is responsible for the registration, management and maintenance of the property registry of South Africa. Even in instances where a transaction is exempt from transfer duty, the SARS exemption receipt from SARS must still be provided to the Deeds Office.

As part of its continuing data-focused approach, SARS is making use of the information that it has on hand, and taxpayers that do not declare their rental income timeously are likely to find their non-compliant behaviour coming to light. Rather than hiding the income, it is recommended that taxpayers and tax practitioners declare the requisite income, and rather spend their time wisely, investigating and preparing proof of the expenses that may be claimed against the rental income earned.

2. Confirmation of the EMP501 reconciliation dates

SARS confirmed that the 2023 annual employer reconciliation period will commence on 1 April 2023 and close on 31 May 2023.

The EMP501 reconciliations will cover the period 1 March 2022 to 28 February 2023. Employers must reconcile the monthly EMP201 submissions and payments with the tax values of the final IRP5/IT3(a) tax certificates, to ensure that accurate information is available to SARS for the pre-population of the ITR12 returns in July.

Before attempting to submit the reconciliations, employers are advised to download the latest e@syFile version which contains all the updated codes and validation rules.

3. The highly anticipated new dispute resolution rules are officially promulgated

On 10 March 2023, the new dispute resolution rules were promulgated into law in terms of section 103 of the Tax Administration Act, No. 28 of 2011 (the TAA).

The rules, which were updated for the first time since 14 July 2014, were brought into effect immediately.

The main and most significant change to the rules is the period within which a notice of objection may be submitted to SARS; the period was increased from 30 days to 80 days. However, the period within which SARS must respond to the taxpayer remains unchanged.

4. Treasury to release draft legislation on the solar (PV) panels outside of the normal legislative cycle

National Treasury published the Frequently Asked Questions (FAQ) on the Solar Panel Tax Incentive for Individuals to help individuals in their immediate decision making by providing the basic characteristics and requirements for the incentive announced by the Minister of Finance on 22 February 2023.

Ordinarily, the draft Tax Amendment Bills are released for comment in July/August of each year, finally to be promulgated into legislation in January of the following year. However, the intention is for the rebate to apply to qualifying solar PV panels that are brought into use for the first time in the period from 1 March 2023 to 29 February 2024.

It follows that some of the unanswered questions need to be addressed by National Treasury before taxpayers will make use of the incentive en masse. It is understood that in order to assist with the uptake of the incentive, National Treasury intends to release draft legislation on the solar panel tax incentive for individuals outside of the ordinary legislative cycle.

5. Focusing on travel allowances for the new tax year

Taxpayers relying on a travel allowance to partially fund their business travel should take note of SARS’ 2023/24 Travel eLogbook, which was published on 16 March 2023.

Although taxpayers do not have to use the SARS format, it is useful to consider the type of information and details that SARS requires to prove business travel.

Many SARS audits lay in dispute based on travel logbooks that just did not measure up to SARS’ scrutiny.

6. Diesel fuel levy refund for food manufacturers

In 2000, the diesel refund system was implemented to provide full or partial relief for the general fuel levy and the Road Accident Fund (RAF) levy to primary sectors. The diesel refund system was put in place for the farming, forestry, fishing and mining sectors.

However, considering the current energy crisis, the government is proposing a similar refund on the RAF levy for diesel used in the manufacturing process of foodstuffs.

This is inclusive of costs incurred in the running of a generator, power a boiler or any other part of your production process. This relief is implemented to limit the impact of power cuts on food prices.

Therefore, on 10 March 2023, SARS published the draft amendment to Part 3 of Schedule No. 6 that relates to the insertion of Note 14 and refund item 670.05/00.00/01.00 for public comment.

Taxpayers that intend to claim this relief will be required to complete the prescribed DA 66 form together with all necessary supporting documents in order to lodge a successful claim.

Notwithstanding the fact that the refund provision will be implemented for two years with effect from 1 April 2023 until 31 March 2025, taxpayers will be required to keep records for 5 years as taxpayers may be exposed to audits and penalties for 5 years after the aforementioned end date.

The refund payments will take place once the system is developed. More details on the proposed changes are available below.

- Domonique Ramos | 03 April 2023