Industry updates | December 2021

Please take note of the following industry updates that may be relevant to you and your business.

COMPLIANCE AND ADMINISTRATION

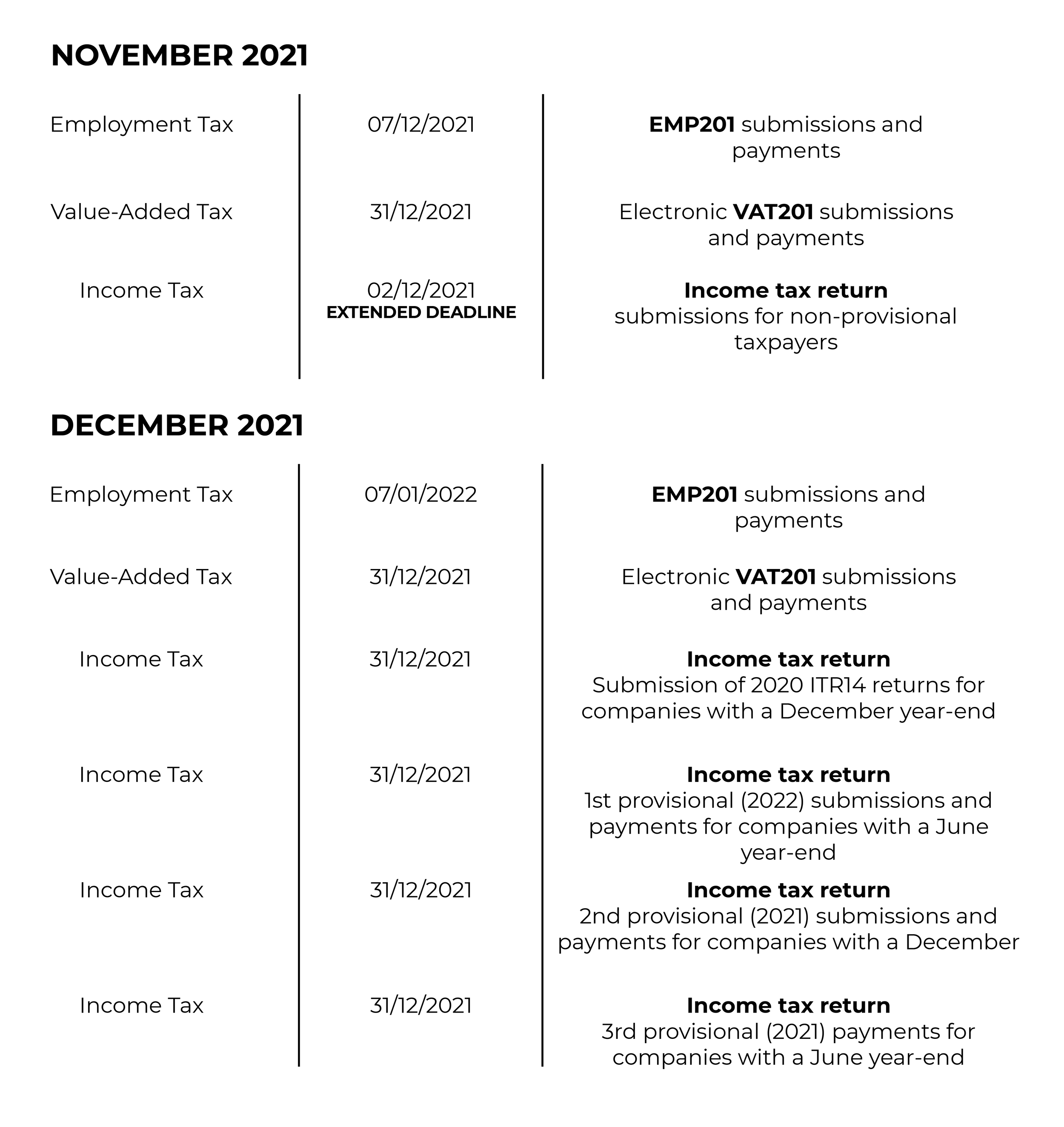

Due dates for reporting and payments- November and December 2021:

*As our offices are closed from the 15th of December 2021 until the 12th of January 2022, please ensure that all December statutory returns and payments are submitted timeously to avoid penalties and interest being levied.

TAX ADMINISTRATION

1. 2021 Income Tax filing season

SARS announced that the Filing Season 2021 submission deadline had been extended from 23 November 2021 to 2 December 2021.

SARS acknowledged the systemic issues experienced during the course of the filing season as well as the impact that loadshedding has had on taxpayers’ ability to submit their income tax returns. As a result of the deadline extension, the implementation of the administrative penalties levied for the late submission of the income tax return has been moved to January 2022.

Therefore, an income tax return submitted after 2 December 2021 by a non-provisional taxpayer will be subject to the administrative penalty for late submission of the return.

2. Reduction in income tax rate for Companies

The company tax rate will reduce to 27% for years of assessment commencing on or after 1 April 2022.

3. Effective rate for more than one annuity income or annuity and salary

The recently introduced legislation allows SARS, with effect from 1 March 2022, to determine an effective rate of tax for a taxpayer in respect of the combined employment and pension sources of income reflected on IRP5/IT3(a) certificates. SARS is enabled to issue a tax directive to retirement fund administrators to apply an effective PAYE withholding rate.

The effective employee’s tax withholding rate is applicable to the following pension/ annuity income sources only:

• Pension (income source code 3603)

• Annuity from a Retirement Annuity Fund (income source code 3610)

• Purchased Annuity (income source code 3611)

• Annuity from a Provident Fund or a Provident Preservation Fund (income source code 3618).

Clients that may be affected from 1 March 2022 are advised to discuss the effect with their tax practitioners before the effective date since some clients may experience a cashflow shortfall as a result.

4. Legislative interpretation

New Binding General Rule:

BGR 57: On 20 October 2021, SARS released Binding General Ruling (BGR) 57 that considers whether the term ‘consideration’ includes an amount of transfer duty for the purposes of calculating a notional input tax deduction on the acquisition of second-hand fixed property.

Summary: “The term “consideration” as defined in section 1(1) does not include any transfer duty imposed under section 2 of the Transfer Duty Act. As a result, the amount of transfer duty paid or payable by a vendor to acquire second-hand fixed property for taxable purposes cannot be included in the calculation of any notional input tax deduction which may be available to that vendor under section 16(3)(a)(iiA) or 16(3)(b)(i).”In both scenarios, a Request for Remittance (RFR) together with all the relevant information and supporting evidence can be submitted to remedy penalties and interest levied by SARS.

5. SARS is feeling enthusiastic

The Commissioner of the South African Revenue Service, Mr Edward Kieswetter, recently told parliament that SARS is feeling enthusiastic and encouraged by the measured progress in rebuilding SARS as an institution that is transforming itself into a “SMART SARS.”

SARS has collected more than R1.55 trillion at gross, which comprises of a net of R1.25 trillion of the revenue estimate and that is R38 billion more than the revised estimate. Refunds paid amounted to R300.6 billion, which is R20 billion more than 2019/2020.

The specific compliance interventions used to detect and deter non-compliance yielded R172 billion, which shows room to improve compliance levels across all tax types. This dovetails with SARS’ strategic objective of making it costly for those who are wilfully non-compliant.

In addition, R38.9 billion had been granted in Covid-19 relief measures and trade to the value of R2.6 trillion had been facilitated in accordance with the SARS mandate.

Kieswetter confirmed that tax compliance levels were under strain, with a composite compliance level of 62.61%, compared to the previous year of 65.05%. The Public Confidence Survey point to favourable preference of tax morality but that has not seen an appreciable rise in compliance.

He said the tax base was broadening with 1.6 million taxpayers added to the SARS tax register that resulted in R4.6 billion added to the net collections for the year under review.

SARS’ strategic objective to make it easy and simple for taxpayers to comply has also yielded impressive results: 86.3% of SARS interactions done through digital channels such as eFiling.

The Commissioner warned however that the impact and prevalence of corruption and waste was not helpful in enhancing tax morale within society.

In addition, 83.2% of standard taxpayers (3.4 million taxpayers) had received auto-assessments based on third party data available to SARS. All taxpayers needed to do was to click accept or edit. The effectiveness of these channels are also indicated by the fact that R1.55 trillion was collected via eFiling.

SARS’ enforcement efforts were also yielding results in a difficult and challenging terrain. These efforts recovered R147 million from PPE fraud and there was a conviction rate of 96% rate through collaboration with the NPA. The organization is also working with all other enforcement agencies as well as other government agencies.

The newly launched High Wealth Individual Segment has written 1400 direct letters to wealthy individuals and 275 have already been reviewed. Equally, SARS has also detected 26 000 unregistered taxpayers who have financial assets with economic activity in excess of R1m.

A focus area has been the compliance levels of the various segments, such as Employers; SMME; Large Businesses & International and High Wealth Individuals. In addition, compliance levels of tax products such as PAYE, CIT has been a concern, and SARS has embarked on focused programmes to address this trend.

The Commissioner said, “in order to deliver on its comprehensive programme and despite the financial constraints, SARS is investing 3% of its budgeted resources in its modernization programme so that it can remain abreast in a fast changing technological space”.

In conclusion he expressed his heartfelt thanks to SARS staff for their inestimable support in discharging the organization’s mandate. In the same vein, he apologised to taxpayers who may have been unable to transact with the organization due to system challenges.

Domonique Ramos | 1 December 2021